Our latest stories

.jpg)

What’s Driving the Rise of European M&A in 2025? Outlook and Opportunities for CEE Founders & Investors

Global slowdown, but Europe challenges the trend

H1 2025 saw a 9% global drop in deal volumes, even as deal values surged by 15%, driven by bigger, high-conviction transactions. Europe, however, is challenging that global trend – based on Pitchbook data:

- 10,274 M&A deals totalling over $516 billion were completed—marking the highest deal count in more than a decade.

- Q2 alone saw $256.3 billion in deal value and 5,205 transactions, underlining sustained momentum.

Meanwhile, Pitchbook also reported that Europe led the globe in private equity exits during H1 2025, surpassing North America in deal count.

What is driving deal activity in Europe?

Several factors explain Europe’s resilience in H1 2025 and support a positive outlook for H2:

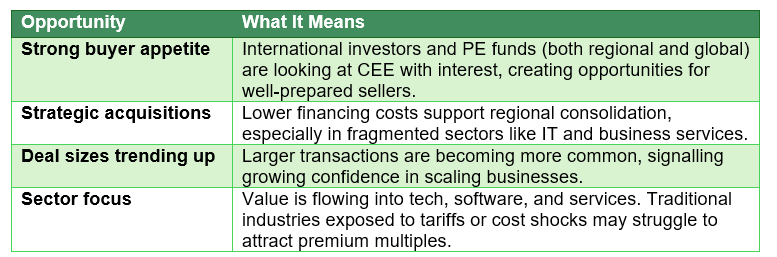

- Valuation gap vs. US.: European companies are still priced lower than US peers, which draw interest from strategic and PE buyers.

- Financing advantage: The ECB cut rates twice this year, while the US Federal Reserve kept steady. Lower financing costs support both dealmaking and valuations.

- Sector focus: Tech, IT services, and software continue to attract the most activity, while energy, automotive, and chemicals remain under pressure from tariffs and higher input costs.

- Sustained appetite from non-European acquirers: PitchBook data shows that despite softer volumes in recent years (compared to a big boom in 2021-22), overseas buyers continue to deploy significant capital into European targets, with $114.9B already recorded in 2025.

Snapshot of CEE: Strategic opportunity and confidence

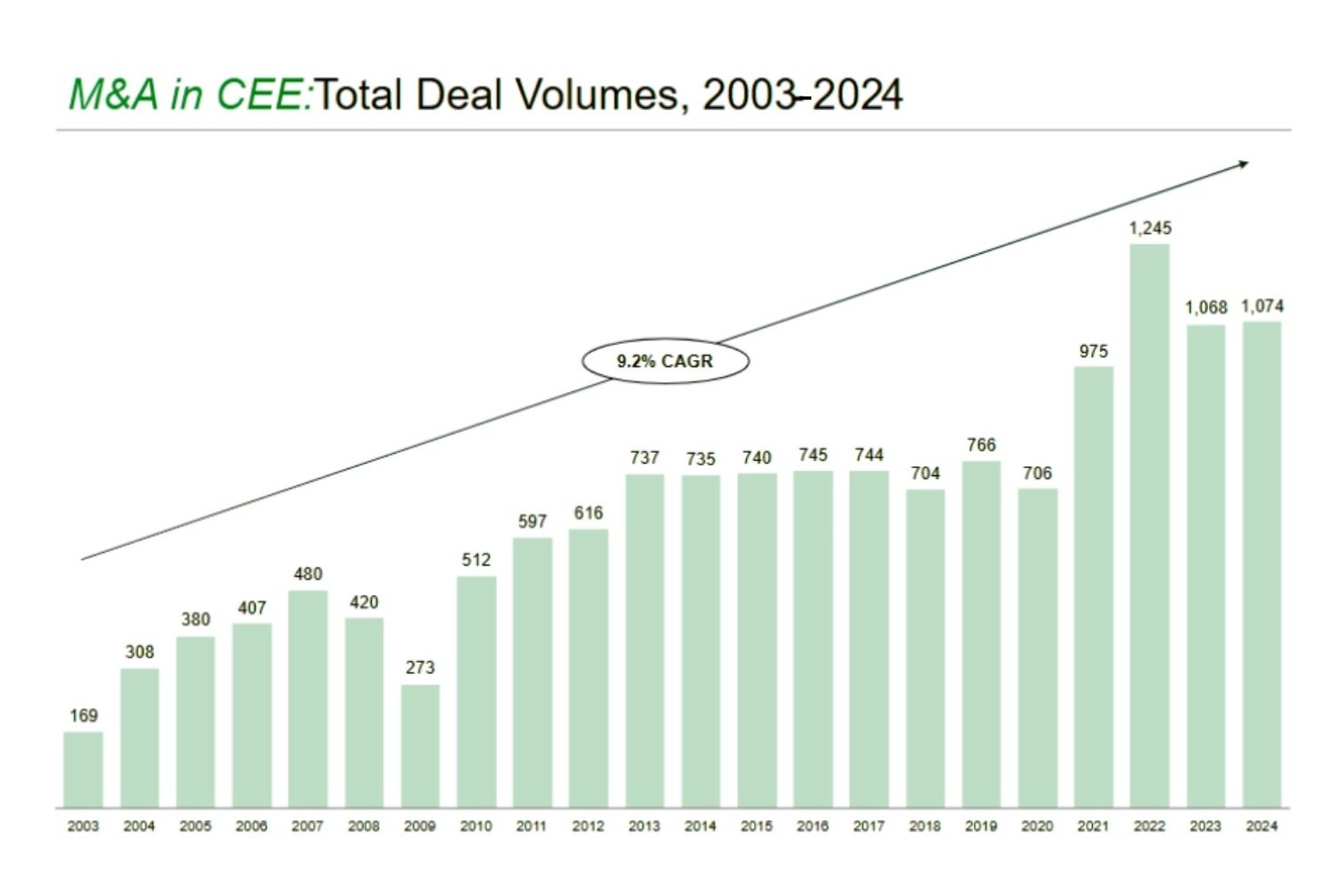

Looking back to the M&A history of the region, MergerMarket analysis shows a strong upward trend in deal volumes across the CEE region since 2003, growing from 169 deals in 2003 to 1,074 in 2024. It represents a 9.2% compound annual growth rate (CAGR). After a peak in 2021 (1,245 deals), volumes slightly declined but have stabilized above 1,000 deals annually in the past three years, signalling sustained transactional activity in the region that seems to be progressing in 2025.

Coming back to 2025, CEE continued to remain stable on sell-side activities, while buy-side transactions went up 3% in the beginning of 2025, according to Dealsuite. In comparison, the UK & Ireland (+8%) and the Netherlands (+6%) saw stronger buy-side momentum, while DACH (–3%) and France (–6%) experienced declines.

H1 2025 already saw notable CEE tech transactions, such as the acquisition of Poland’s Dealavo. EY also reported that while deal count in the region slowed, deal values jumped by 113% YoY, with mid- to large-scale tech transactions doubling. This shows CEE is no longer just a talent hub – it’s delivering real exit opportunities.

Across these deals, three patterns stand out:

- Exit timing: founders sold after proving €10–20M ARR, before heavy international expansion costs kicked in.

- Strategic logic: Western buyers used CEE acquisitions to add tech modules or engineering capacity faster and cheaper than building in-house.

- Fund dynamics: regional VCs raising new funds pushed for realizations, driving proactive sale processes.

Sector-wise, CEE follows broader European patterns:

- Business services and industrials lead in transaction volume.

- Software and IT services are particularly attractive thanks to strong talent pools and digitisation trends.

- Traditional sectors like automotive and construction remain active but face global trade and cost pressures

What does this mean for founders and investors active in CEE?

For founders, this means waiting for the “perfect moment” risks missing the buyer’s window. For investors, it underlines that CEE scale-ups are now proven exit stories, with buyers actively scanning the region. Preparation – in governance, metrics, and buyer relationships – will determine who captures premium multiples in the next wave.

Outlook for H2 2025: Optimism with cautiousness

Looking ahead to the second half of 2025, these are what we can expect:

- Deal flow is expected to stay strong, particularly in tech, infrastructure and services.

- More private equity funds may sell their portfolio companies in H2, as they look to return capital to investors and take advantage of active buyer interest

- Regional consolidation and possible megadeals will likely remain part of the picture, even as many founders continue to wait for the “perfect timing” to sell.

- Uncertainty remains, with tariffs, geopolitical risks and long-term rates still weighing on confidence. Yet, as PwC notes, “uncertainty may be the new constant”, and dealmakers who prepare strategically will outperform.

Summary

H1 2025 proved that European M&A is resilient, with deal flow at decade-high levels. For CEE, rising buy-side demand and steady valuations mean that both founders and investors have a real window of opportunity in H2. Let’s see at the end of the year how it turns out.

How Absolvo can support you in your M&A strategies?

At Absolvo, we know that preparation and the right partner can make or break a deal. Our experience shows that founders who prepare well in advance (often 2–3 years before a potential exit) and strategically position their business while accessing the right investors can achieve 2-3x better valuations and receive more competitive offers. With decades of M&A experience and a network of 28,600+ active investors, Absolvo help you navigate these times with confidence, because now may be the best time to act.

Reach out if you want to talk to us and prepare together for mastering your M&A strategy and exit opportunities.

Sources:

Pitchbook Report 2025

Mergermarket Report 2025

PwC Report 2025

Dealsuite Report 2025

M&A Trends in Central and Eastern Europe: What Recent Tech Acquisitions Reveal from 2025 H1

Pattern #1: Private Equity Fuels Strategic Expansion in CEE Tech

PE-backed multi-strategy execution

Like in a recent deal, where Hg is supporting JTL in advancing its SaaS product development while also enabling the company to expand regionally and into adjacent sectors, PE investors’ arekeen to find good targets. The acquisition of Dealavo is a prime example of these strategic objectives in action, just like Revolution Software’s by Seyfor, backed by Sandberg Capital and many more. This pattern is increasingly visible across the region; among our clients we see many CEE-based companies being approached by private equity-backed buyers.

PE backing fuels acquisition-led expansion

Since securing investment from Hg in Q4 2023, JTL-Software has completed five acquisitions - a notable shift from its previous track record of zero deals. With Hg’s capital and strategic support, JTL is aggressively growing its capabilities, market reach, and competitive position. Since Exadel partnered with Sun Capital Partners, the company has executed multiple acquisitions across Bulgaria and Poland. These moves expand its delivery footprint and align with a broader strategy to scale rapidly through inorganic growth

Takeaway

When a private equity firm backs up your potential buyer, it may be the right time to consider a transaction with them. PE involvement often signals future consolidation, strategic add-ons, and regional platform-building. Growth pressure and financing is given. We are directly involved in such transactions, often negotiating with private equity firms on the other side of the table. We’ve seen cases when a PE-backed company executed 25+ deals in 1,5 years, that highlights the pace and intensity of buy-and-build strategies once the capital and mandate are in place.

Pattern #2: Complementary Software Acquisitions Drive Product Innovation

Enhancing product offering

JTL strengthened its cloud-native multichannel suite by acquiring Dealavo’s advanced pricing and market intelligence solutions. This enhances JTL’s value proposition to existing clients and supports upselling within its ecosystem.

AI capabilities as a differentiator

Anthill, acquired by Exadel, brings significant expertise in data, AI, and enterprise software development. These capabilities align with Exadel’s strategy to deliver innovation-focused,high-value digital services.

Strategic fit

These buyers are increasingly focused on acquiring companies that complement their core platforms. By integrating specialized capabilities like pricing automation, data engineering,or cloud-native tools, acquirers can quickly expand their value offering. Simple as that: the buyer can offer additional features, modules or software to their existing client base almost immediately and start generating revenue (and profit) from day one.

Pattern #3: International Expansion Through CEE Tech Hubs

Global expansion through local leaders

Dealavo’s presence across 30+ markets supports JTL’s regional expansion goals, especially in the DACH region.

Cross-border scale

Savangard, acquired by Digia, already generated nearly 30% of its revenue outside Poland, helping Digia diversify risk and broaden its reach across Europe.

CEE as a delivery hub

With the acquisition of Anthill, Exadel makes Bulgaria its second-largest European delivery location. Buyers increasingly recognize CEE’s importance for nearshoring, talent access, and strategic delivery capacity.

These deals can illustrate a larger trend: once acquirers become active in the CEE region, they are more likely to pursue follow-on acquisitions due to growing familiarity with the legal and business environment.

Pattern #4: Smart Valuations in CEE Tech M&A Deals

Attractive pricing dynamics

Digia’s acquisition of Savangard at approximately 6.5x EBITDA reflects a disciplined yet strategic approach. This valuation is below the 8-12x EBITDA median typically observed in the regional IT services space.

Takeaway

High-quality targets that demonstrate growth, profitability, unique capabilities, visionary management and international reach continue to attract strong valuations, especially when they fit into larger strategic narratives.

Pattern #5: Retaining Local Talent and Brands in Regional Deals

Preserving team and identity

Savangard will continue tooperate as a subsidiary under Digia, retaining its leadership and brand (a model that supports client trust and post-deal stability).

Gradual integration

Anthill will initially operate as “Anthill by Exadel,” signaling respect for the company’s culture and relationships while ensuring alignment with the parent company’s global operations over time.

Takeaway

As per our experience, more and more acquirers – particularly in tech and innovation-driven sectors – are shifting away from fully integrating acquired teams to preserve innovation, retain talent and reduce cultural friction. Research also supports this trend,highlighting that light-touch integration and portfolio models help maintain agility and morale while enabling faster realization of value. Forcing integration can undermine the very qualities that made the target company attractive in the first place.

Pattern #6: Rise of the vertical software integrators

A new type of buyer is becoming increasingly active in CEE: vertical software integrators. These firms typically focus on a specific or narrow set of industries, and their goal is to build platforms of industry-focused software and services that can scale internationally. As global economic uncertainty led many strategic buyers to become more cautious in recent years, these specialized players have grown bolder. From the UK to Dubai, and from Germany to Poland, we're seeing more of these integrators actively exploring the region, engaging in deals and establishing a broader presence in CEE. We’ve seen this trend firsthand. Our team recently closed two transactions involving vertical software integrators, and we’re tracking several more in the pipeline.

Closing remarks

The Central and Eastern European technology M&A market is clearly evolving. International buyers - both private equity-backed and strategic - are actively acquiring regional companies to access talent, specialized capabilities, IP, and scalable platforms.

Successful targets often exhibit a combination of international client exposure, cloud or AI-enabledservices, globally tested products, and a strong niche focus. As more capital flows into the region and acquirers grow increasingly comfortable with local dynamics, we anticipate continued momentum in the CEE deal market.

About Absolvo

Absolvo specializes in M&A and growth financing, backed by 380+ completed deals collectively in the Central and Eastern European region. We support technology companies through strategic exits, private equity transactions, and cross-border growth initiatives. If you are considering an exit or a strategic partnership, our team is ready to help you prepare and position your business toward an exit that could deliver 3–5x its fair value.

Analyzed companies:

JTL Software - ERP-Software von JTL: Smarte Lösungen für den E-Commerce

Hg Capital - Hg | Building enduring software and services leaders | Hg

Dealavo - Competitor price tracking software & price analysis - Dealavo

Savangard - Homepage - Savangard

Anthill - Home - Anthill

Exadel - Enterprise Software Development and Consulting | Exadel

Digia - https://digia.com/

Sources:

Market Screener

Mergermarket

McKinsey Report 2022

PwC Report 2024

Channel E2E

.jpg)

Central and Eastern Europe: A rising force in global tech and innovation

1. Economic and Digital Convergence

The CEE region has a total population of more than 130 million people – higher than the sum of DACH region and Sweden’s –, and accounts for approximately 30% of the European Union's total population of approx. 450 million. The region’s combined GDP was more than $2 trillion in 2023, close to Canada’s total ($2.24 trillion).

The economic progress of the CEE region is unmistakable. Countries such as Hungary, Czech Republic, Slovenia, and Poland have significantly improved their GDP per capita since 2018, steadily closing the gap with the EU average. This trend reflects broader economic development, increased purchasing power, and improving business conditions across the region.

Annual revenue growth in IT services in the next 5 years is expected to exceed the EU average in every major CEE country, that forecasts a strong and sustained digital boom.

2. A Thriving ICT sector with strong foundations

The ICT sector plays a central role in the region’s economic future. The CEE region is rapidly advancing as a digital hub, with countries like Croatia, Czechia, and Estonia exceeding the EU average. The increasing investments in digital infrastructure such as data centers and cloud services highlight infrastructural development while EU-backed initiatives alongside regional collaborations also underscore how regulatory frameworks drive growth in the region.

In some CEE countries like Bulgaria and Hungary, the value added by the ICT sector already exceeds the EU average. The region boasts a higher share of ICT employment and nearly double the number of ICT companies per 1,000 inhabitants, showcasing an increasingly vibrant tech ecosystem.

Supporting this momentum is a deep pool of local talent, tech engineers ranked top performing based on various rankings. The proportion of ICT graduates across CEE countries consistently surpasses the EU average.

Romania leads the way, with over 6% of graduates specializing in ICT fields, a key factor in attracting tech investment and innovation.

Furthermore, labour costs remain significantly lower in CEE than in Western Europe. In 2024 the hourly labour costs across the region are often under €20, while IT salaries are more than 30-40% lower than in Western tech counterparts like Germany, the Netherlands or Luxembourg. For global tech firms, this combination of affordability and quality talent is hard to ignore.

Consequent to the recent Ukrainian-Russian war, the CEE tech pool is experiencing a large influx of IT talent relocating from Ukraine, which boasts one of the largest developer communities in Europe.

3. Global Players and CEE

Recently the CEE region has become a magnet for multinational corporations and global tech leaders, already drawn many multinational companies like Microsoft, Google, Intel, Oracle, and HP in the past to establish a strong presence here.

OpenAI CEO Sam Altman has publicly praised Poland’s engineering talent, calling it crucial to OpenAI’s success. OpenAI’s plans to open European headquarters in Poland signal growing confidence in the region’s innovation potential.

4. Tech sector: the heart of M&A activities in the region

The technology M&A sector plays a key role in the region, accounting for 15-25% of all completed deals in CEE and contributing 10-30% of the region's total deal value through the years. Western investors – especially from the US, Germany, and the UK – dominate inbound deal activity, drawn by strong fundamentals and a high return potential.

CEE startup exits have quadrupled over the past decade,

including Croatia’s Photomath acquired by Google, and Bulgaria’s Pliant bought by IBM.

In 2023, nearly 40% of funding came from outside the region, especially from Western Europe and North America, increased from 2021’s figure of 30%.

AI has become a key focus – 45% of all funding in 2023 was directed toward AI-related startups. Vertical sectors such as enterprise software, security, fintech, and robotics are among the most heavily funded.

UiPath’s Global success – a relevant example

Romania-based UiPath is a prime example of the CEE region’s tech potential. Founded in 2005, the company transformed from a small RPA startup into a global automation leader. Backed by early investment from CapitalG (Google’s venture arm), UiPath rapidly expanded, acquired multiple companies, and eventually launched a $1.3 billion IPO on the NYSE—one of the largest US software IPOs in history.

Today, UiPath serves clients in over 30 countries and employs more than 4,000 people globally, embodying the rise of CEE as a launchpad for world-class tech firms.

Conclusion

Central and Eastern Europe is not just an emerging player, but a rising future force in the global technology arena. The region combines fast-growing economies, digital readiness, abundant technical talent, low operational costs, and increasing investor confidence. With a supportive policy environment, strong startup activity, and a proven track record of scaling global tech successes, the CEE market is set to outpace much of Europe in digital transformation.

For companies, investors and entrepreneurs seeking high-growth opportunities, CEE stands out as one of the most promising frontiers in the global tech landscape.

Sources:

https://databank.worldbank.org

When and why should a scaleup get a private equity on board and what does it change?

Why Private Equity? Timing, Strategy, and Opportunity

Both companies entered the PE universe with different motivations, but a shared recognition that scaling sustainably required more than own capital available and organic growth.

For WTS Klient, the trigger was internal due to different visions. This divergence created a natural inflection point where bringing on an investor provided liquidity and strategic alignment.

In Finshape’s case, the PE partnership emerged during a moment of strategic ambition. After a management buyout, the team saw an opportunity to merge with a similar Czech-based company. This merger required immediate capital and the ability to execute a cross-border M&A—something only a capable PE partner could support.

In both cases, the decision wasn’t about a lack of ambition but about enabling the next phase of that ambition through structure, capital, and expertise.

What Changes When PE Enters the Room?

While financial resources were a clear value-add, both founders emphasized the operational transformation that comes with private equity investment. Reporting, strategic planning, and performance tracking became more formalized and more demanding.

“PE didn’t mean losing control - but it did mean more structure, more KPIs, and real accountability.”

said Jozsef Nyiri, referencing their use of the 'Rule of 40' to combine profit margins and growth rate to benchmark success.

For WTS Klient, it meant upgrading internal systems and introducing new layers of professional management to support a tripling in headcount over just a few years.

Tamas Gyanyi added that investor oversight brought more than just pressure – it brought professionalization.

“We became more efficient. We didn’t just grow in size—we grew up as an organization.”

he said.

Integration and Culture: Growth with a Human Lens

With private equity often comes consolidation—and with that, the challenge of integrating teams, processes, and cultures. Both WTS Klient and Finshape experienced this firsthand.

WTS executed multiple acquisitions in short succession. While this enabled rapid expansion, it also introduced high staff turnover in the acquired firms. Rather than see this as a setback, Gyanyi framed it as an opportunity to re-staff with future-oriented, culturally aligned professionals. The firm also launched an employee ownership program to retain top talent and strengthen internal alignment with long-term goals.

Finshape invested the time by face-to-face interactions and fostering mutual understanding, the firm gradually aligned its leadership culture.

In both companies, a central theme emerged: preserving core values amid scaling requires intentionality and communication. Social initiatives, direct engagement from top leaders, and open-door practices helped maintain a sense of unity even as operations expanded.

The Role of AI and Digitalization in Future Growth

As both companies look ahead, technology and AI are expected to play a larger role in driving efficiency and profitability. WTS Klient is already leveraging AI through its global network’s digital platform, which supports faster, semi-automated tax advisory responses. The firm also anticipates AI playing a bigger role in payroll and HR automation, reducing the need for manual roles and.

“We’re already using AI to semi-automate tax advisory. In payroll and HR, it’s going to help us scale and enhance EBITDA margins.”

said Tamas Gyanyi.

At Finshape, digitalization is embedded in the product, but operational AI initiatives – like measuring developer efficiency or improving test case throughput – are also becoming areas of focus. The investor’s support in bringing financial and analytical rigor is seen as a key enabler of such innovation.

“Even internally, we use AI to track developer efficiency or speed up test cycles—it’s becoming part of our operating rhythm.”

added Tamas Nyiri.

Balancing Investor Goals with Founder Vision

Despite the operational enhancements and strategic benefits, the founders acknowledged that conflict is sometimes part of the journey. Differences often arise in areas like sales strategy, where investor-level perspectives may not always align with on-the-ground realities. However, both founders expressed appreciation for the tension, as it often results in better outcomes when managed through transparency and mutual respect.

They also reflected on the personal growth required to operate in a PE-backed environment. Learning integration strategy, managing complexity, and accepting board-level scrutiny are all part of the evolution from founder to scale-up leader.

Crucially, both companies were able to retain their entrepreneurial spirit—not despite the investor, but often because of the structure and discipline the investor introduced.

“Sales is like football – everyone thinks they’re a coach.” Jozsef joked. “There were debates, but constructive ones. And we’re better for it.”

“I had to learn integration, HR, investor reporting – things I never planned for. But I’m a better leader now because of it.”

Tamas reflected.

Final Thoughts

The session concluded with a sense of measured optimism and maturity. For both WTS Klient and Finshape, the journey with private equity is not just about funding expansion, it's about scaling with intention, structure, and cultural integrity.

Private equity is often viewed through a transactional lens, but this panel made clear that it can be a deeply transformative partnership—one that helps companies not just grow faster but grow better.

As both founders continue executing their buy-and-build strategies, the lessons from this session reinforce a broader truth: when aligned with the right partner, private equity can be a powerful force for long-term, people-centric value creation.

Read the Investor perspective here.

If you're looking to understand how the private equity space works and who the active players are, reach out and let’s have a chat.

What is the outlook for 2025-2026 in private equity deals?

Outlook for 2025–2026

The session opened with a macro-level view of the market. Following a period of inflated valuations and unpredictable fundraising conditions, investors now see stabilizing trends and greater clarity for deployment.

According to recent figures, the volume of CEE PE buyouts remained relatively stable compared to previous years, with approximately 150 deals executed, similar to 2022 and 2023. On the exit side, the number of PE-backed exits in the region saw a slight increase, which is a promising sign for liquidity. Although, deal values again fell, which aligns with global observations that valuations have normalized from the overheated levels of 2021 and early 2022.

Despite the challenging environment, several private equity firms remained highly active in the CEE region (including our guest, Abris Capital). This continued presence of leading firms underscores the long-term strategic commitment to the region, even in a cooling market.

The outlook among professionals remains cautiously optimistic. As noted in a supporting survey, 91% of respondents expect PE activity to increase in 2025, with strategies focusing on market consolidation and buy-and-build approaches. However, macroeconomic factors (such as geopolitical instability and slowed economic growth) are expected to weigh heavily on deal-making strategies in the near term.

“There’s been a consolidation in valuations… targets are no longer overpriced, which is finally making room for deals again”

noted Tomasz Hajduk from Abris Capital.

Both firms confirmed from their own experience that there is a gradual reactivation in the market, in line with broader expectations. This creates a more favourable environment for executing deals, especially for funds already well-capitalized and experienced in CEE dynamics.

Platform Deals and the Buy-and-Build Model

A core focus for both Abris and Provectus remains the buy-and-build strategy, which they view as the most effective approach to value creation in fragmented sectors. Provectus has leveraged this model across several verticals, particularly healthcare, where they’ve built leading regional players through a series of add-ons.

Rather than passive acquisitions, the emphasis is on active operational development—professionalizing management, centralizing procurement, and investing in shared services. The result is not just revenue growth but the creation of platform companies that are structurally scalable and strategically differentiated.

“We focus on fragmented markets where you can consolidate smaller players into a dominant group – that’s where real value creation happens”

said Marko Galic, referencing Provectus Capital's success in healthcare.

Similarly, Abris employs buy-and-build as a foundational strategy, but also looking for transformational deals.

Their portfolio includes businesses that have undergone full-scale transformation. Not just geographic expansion but business model reinvention. This includes shifting traditional service companies toward digital, tech-enabled revenue models, which provides multiple levers for future growth and exit readiness.

Founders as Partners: Transition Planning Is Key

For PE firms, the acquired company’s team and management are key, and both firms approached the founders and management with a clear, structured process. Founders are typically retained to preserve institutional knowledge and ensure continuity. However, investors expect early conversations around succession planning and the professionalization of leadership.

Rather than abrupt changes, the model is built around gradual transition—starting with strategic hires such as CFOs and COOs who can prepare the business for its next phase of growth or eventual sale. The ability to manage this transition smoothly is seen as a key differentiator in the CEE context, where many companies are still founder-led and under-resourced in senior management.

VCs Turning to PE: A Growing Trend

One emerging dynamic in the region is the increasing number of VC-backed companies seeking exits through PE. As capital availability in venture markets contracts and IPO paths remain limited, many startups that have matured but not scaled explosively are looking to PE as the next logical step.

“We’ve had VC-backed firms approach us after growth slowed. We step in with majority control, operational expertise, and turn them into profitable add-ons.”

said Tomasz.

This is particularly true for companies that have strong fundamentals but need operational discipline and a route to profitability. PE firms see these as attractive add-on candidates or, in some cases, small platforms. While these opportunities require a mindset shift—from founder control to PE governance—they are becoming more frequent and viable as the ecosystem evolves.

ESG and AI: Practical Applications in Value Creation

Environmental, Social, and Governance (ESG) factors are no longer just compliance items, they are fully embedded in investment processes. Both firms conduct ESG due diligence on every deal and apply structured improvement targets post-acquisition. ESG performance is now directly tied to incentives and increasingly considered essential for any successful exit, especially when selling to Western strategic or financial buyers.

“Our portfolio companies report on ESG alongside financials and management bonuses are tied to those targets.”

said Marko.

On the AI front, investors are selectively integrating tools for market mapping, reporting automation, and portfolio company operations. While proprietary AI development remains limited, commercial tools with embedded AI capabilities are reducing manual workloads and improving operational efficiency. Use cases, such as content automation for e-commerce platforms, demonstrate how even small innovations can unlock significant productivity gains. At the same time, they made it clear that despite AI’s great potential, they won’t act like VCs. For them, early-stage deals are off the table, as their investment thesis and mandate remain firmly rooted in the private equity approach.

Closing Reflections

The session concluded on a grounded but positive note. Both Hajduk and Galic emphasized that while uncertainty remains a feature of today’s markets, it also creates opportunities for investors who stay disciplined, focused, and adaptable.

In their view, private equity in CEE is entering a new phase—one that favors strategic clarity over market timing, active value creation over financial engineering, and partnerships with entrepreneurs who are ready to evolve.

As 2025 unfolds, the message from leading investors is clear: with the right model, right sectors, and right relationships, CEE remains one of Europe’s most promising regions for private equity success.

Read the Founder perspective here.

If you're looking to understand how the private equity space works and who the active players are, reach out and let’s have a chat.

Decoding CEE M&A: Key Insights into Tech M&A Trends in Central Eastern Europe from H2 2024

Pattern #1: B2B niche targets are attractive for vertical software firms

- Example to highlight:

Upliift, a London-based investor, focusing on European B2B software firms with revenues between €1-25 million acquired SRC, a Slovenian software development firm with over 200 employees and a presence across several countries in the CEE region.

- Pattern explained:

This transaction aligns with a recent trends in the region, where a new class of investors such as Vesta Software Group, Everfield, saas.group, Jonas Software or Constellation (and many more) target cashflow-positive, founder-owned B2B software companies in niche markets. Unlike traditional strategic buyers, these investors prioritize maintaining the independence of acquired companies, fostering growth without full integration.

Pattern #2: Prior partnership with acquirer increases the chances of transaction success

- Example to highlight:

The recent acquisition of Polish companies Mediarecovery and SafeSqr by Dutch firm DataExpert, which was rooted in over a decade of increasingly close cooperation between the two entities. DataExpert has employed a similar strategy in the past, collaborating with Swedish Forensic Experts Scandinavia AB before acquiring them in 2018.

- Pattern explained:

When acquisitions stem from years of cooperation, buyers gain a deep understanding of the target's strengths, values, and potential revenue impact. This prior collaboration can also benefit the target by justifying a higher purchase price, often supported by proven results.

Pattern #3: Private Equity fuels inorganic growth

- Example to highlight:

Software Mind, a Polish software development services provider, backed by Enterprise Investors – one of the largest Private Equity funds in Poland and the CEE region, acquired Gama Software, a software development company based in Romania.

- Pattern explained:

The involvement of PE firms is a key driver of M&A activity in CEE. Companies backed by PE often pursue aggressive buy-and-build strategies to scale and expand. As a result, these companies tend to engage in more acquisitions than their non-PE-backed counterparts, as growth is a key expectation from private equity investors.

Pattern #4: Consolidation is the good old strategy for growth

- Example to highlight:

Bianor Holding’s acquisition of Prime Holding and Digital Lights in Bulgaria demonstrates a strategic move to consolidate capabilities and strengthen competitive positioning in the industry.

- Pattern explained:

Consolidation is a powerful strategy for everyone, in this case, for IT service providers in the CEE region seeking to compete on European and global stages. To effectively challenge larger players in other markets, these companies must increase their size by pooling resources and expertise, allowing for faster scaling. As some CEE firms strive to penetrate these larger markets, size and operational capacity become crucial factors for success.

Pattern #5: Timing can make or break a deal

- Example to highlight:

Moj-eRačun, Croatia's leading provider of SaaS business tools, specializes in digitizing administrative tasks with its flagship product that offers e-invoicing and document management solutions. This product seamlessly integrates with over 400 ERP systems, providing a substantial competitive advantage as Croatia prepares for mandatory B2B invoicing set to be implemented in 2025.

- Pattern explained:

Timing significantly impacts deal success, especially in markets preparing for regulatory shifts. This upcoming regulation is anticipated to drive demand, adding competitive value. The favourable timing and anticipated revenue growth contributed to a noteworthy valuation in the acquisition by Visma, a Norway-based software provider with an existing track record in the region.

Summary

From niche B2B acquisitions to strategic timing, these insights reveal the diverse approaches shaping tech M&A in the CEE region. Understanding these patterns can be crucial for investors and companies alike, as they navigate the unique dynamics of Central Eastern Europe’s evolving tech landscape.

At Absolvo Consulting, we are actively managing transactions for tech and innovation-driven companies across Central and Eastern Europe. Our daily interactions with strategic buyers and private equity firms give us unique insights into investor priorities, emerging investment trends and market dynamics. This helps us gain a precise understanding of investor needs and focus areas, so we can tailor our deal strategies for our client’s projects to meet these specific requirements.

Tech savvy & wealthy: Ranking Europe’s top 10 Private Equity firms by dry powder for tech deals – 2023 Q3 edition

Private equity firms play a crucial role in funding and supporting the growth of companies across industries, including Information Technology and tech-enabled services. In this article, we will explore the top European private equity firms with the largest dry powder and strong focus on investing in tech companies across Europe.

Here we provide an overview of each firm’s investment strategy, their dry powder, and their successful investments and exits, primarily in the tech sector, based on Pitchbook data available until April 2023. The following firms have the capability to offer strategic support beyond capital that are essential for companies aiming for significant growth.

Top 10 European PE firms by dry powder available:

- 10. AlpInvest Partners

Dry Powder: 8.84 billion EUR

HQ: Amsterdam, The Netherlands

Web: https://www.alpinvest.com/

AlpInvest Partners is a highly experienced global private equity firm with a substantial dry powder of 8.84 billion euros, managing an impressive 59 open funds and overseeing assets under management exceeding 60 billion euros. Renowned for its track record of over 1,000 successful investments and a dynamic portfolio of 49 companies, AlpInvest has established a sterling reputation for its acumen in recognizing and allocating capital to cutting-edge enterprises across diverse sectors.

AlpInvest has made astute investments in an array of companies, exemplified by its acquisition of Profi Rom Food, a leading European retail chain based in Romania, in February 2017 for 575 million euros through a co-investment, buyout deal. Additionally, AlpInvest has demonstrated its prowess in the telecommunications sector through its strategic investment of 202 million euros in Euskaltel, a Spanish telecommunications company, in October 2012 as part of a co-investment growth deal. Notably, AlpInvest has played a pivotal role in fostering the remarkable growth of Euskaltel during its ownership tenure, culminating in a successful exit in August 2021 for a substantial 2 billion euros, delivering impressive returns to its investors. Apart from Euskaltel and Profi Rom Food, AlpInvest’s investment history boasts a roster of well-known companies, including Cushman & Wakefield and Avaya.

With a legacy of more than 250 successful exits, AlpInvest has firmly established itself as a trusted partner for generating significant returns through strategic investments and value creation. The firm remains steadfast in its commitment to fostering the growth and development of its portfolio companies and has a proven track record of successful collaborations with visionary leaders in the business world.

- 9. Bridgepoint

Dry Powder: 9.99 billion EUR

HQ: London, UK

Web: https://www.bridgepoint.eu/

Bridgepoint Advisers, a leading private equity entity, has a robust collection of 14 investment funds and oversees an astonishing 40 billion euros in managed assets. Acclaimed for its exceptional talent in discerning and investing in revolutionary companies across a wide range of industries, including the field of information technology, the firm boasts a remarkable history of achievements with more than 600 prosperous investments and a dynamic portfolio of 70 active companies. Armed with a substantial reserve of 9.99 billion euros as dry powder, Bridgepoint Advisers is aptly equipped to seize profitable prospects in the dynamic market landscape. The company primarily invests across four verticals, which are advanced industrials, business and financial services, consumer, and healthcare, with technology as a horizontal connected to everything everywhere.

Among its successful investments, Bridgepoint Advisers acquired Dr Gerard, a Polish food company in October 2013 through an LBO. Additionally, in January 2015, the firm made a successful investment in eFront, a renowned software provider of alternative investment management solutions, with a leveraged buyout worth 430 million euros. During its ownership period, Bridgepoint Advisers demonstrated its expertise in the sector by supporting eFront in achieving substantial growth. In May 2019, the firm successfully exited its investment in eFront for 1.16 billion euros, resulting in significant gains for its investors.

- 8. Nordic Capital

Dry Powder: 14.08 billion EUR

HQ: Stockholm, Sweden

Web: https://www.nordiccapital.com/

Nordic Capital is a distinguished global private equity firm that boasts a dry powder of 14.08 billion euros, managing 5 open funds and holding assets under management worth 25 billion euros. With over 400 total investments and an active portfolio of nearly 50 companies, Nordic Capital has a history of uncovering and placing investments in pioneering, growth-oriented companies across various industries, including information technology. Furthermore, Nordic Capital is dedicated to investing in companies that proactively address global challenges, contribute to building a prosperous society for all, and promote transformative sustainable change.

One of Nordic Capital’s remarkable investments in the IT sector was back in 2012 when it successfully completed a leveraged buyout (LBO) of Itivity Group, a Dutch software and IT services company, valued at 228 million euros. Over the course of nine years, Nordic Capital played a pivotal role in Itivity Group’s growth journey by facilitating the expansion of its product portfolio, customer base, and market position. The result was an outstanding achievement as Itivity Group was eventually sold for a staggering 2.14 billion euros in May 2021, realizing major profits to Nordic Capital’s investors. Besides Itivity Group, the Swedish private equity firm invested in other influential companies, such as Lindorff Group or Bank Norwegian.

Nordic Capital is renowned for its investment approach, which centers on long-term growth and value creation. The firm has established itself as a trusted partner for visionary company leaders who aspire to expand their businesses. Boasting a track record of over 110 successful exits, Nordic Capital has earned a sterling reputation for generating impressive returns for its discerning investors.

- 7. Cinven

Dry Powder: 15.35 billion EUR

HQ: London, UK

Web: https://www.cinven.com/

Cinven, a prominent global private equity firm with an impressive dry powder of 15.35 billion euros, manages seven open funds and oversees assets under management worth more than 30 billion euros. With a robust performance record of identifying and investing in progressive, expansion-minded companies across various sectors, including information technology, Cinven has established itself as a leader in the industry. One of the firm’s current funds has been named a Real Deals ‘Future 40 ESG Innovator’ which underscores Cinven’s special focus on making positive economic, social, and governance impacts through their investments.

Cinven’s extraordinary expertise in the tech sector is proved by several notable investments. One of these was the leveraged buyout of CPA Global, a leading intellectual property management company based in the United Kingdom, valued at 1.14 billion euros in 2012. Under Cinven’s guidance, CPA Global experienced major growth over the course of five years, showcasing Cinven’s ability to create value. In 2017, Cinven successfully exited CPA Global for 2.69 billion. It is a great example of the company’s rich history, which includes around 170 successful exits. Due to this fact, the company has a strong reputation for garnering considerable profits for its investors.

- 6. Intermediate Capital Group

Dry Powder: 22.08 billion EUR

HQ: London, UK

Intermediate Capital Group (ICG) is a highly regarded private equity firm that specializes in investment management and corporate finance. With a significant dry powder of 22.08 billion euros at its disposal, the firm expertly manages 34 open funds and boasts an active portfolio of 70 companies and a staggering 70 billion euros in assets under management. The London-based firm is committed to fostering a future workforce that prioritizes diversity as a core value. In ICG’s 2020 graduate programme, an impressive 63% of participants were female, while 37% identified as belonging to an ethnic minority group. Additionally, the firm actively supports young individuals from underserved communities through various initiatives and programs.

ICG has an exemplary history of prosperous investments spanning various industries, including the lucrative IT sector. In September 2017, the firm co-invested a substantial 1.53 billion euros in Norwegian Visma Group, a leading provider of cutting-edge business software and cloud services, in a secondary transaction. This investment underscores ICG’s astute acumen in identifying companies with innovative products and services.

Furthermore, ICG has a rich history of successful exits, with over 300 notable exits to its name, including the profitable exit of Poland-based media and communication service provider Aster City Cable in September 2011. This remarkable expertise emphasizes the firm’s commitment to delivering outstanding returns for its esteemed investors. ICG’s noteworthy investment in Visma Group, combined with its extensive experience and a history of lucrative exits, positions it as a compelling option for companies seeking exceptional growth and expansion opportunities.

- 5. CVC Capital Partners

Dry Powder: 23.55 billion EUR

HQ: Luxembourg, Luxembourg

Web: https://www.cvc.com/

Renowned for its exceptional reputation and formidable prowess, CVC Capital Partners stands as a distinguished private equity firm with a noteworthy dry powder of 23.55 billion euros dispersed among its seven active funds. The company prides themselves on integrating ESG within their operations and investment processes. With the aim of producing sustainable value for their portfolio companies and investors, the firm had near 1,000 total investments before, and currently manages over 150 thriving organizations that collectively amass a mammoth 137 billion euros in assets under management.

The firm’s unparalleled expertise in the ever-evolving realm of information technology renders it an irresistible choice for visionary leaders in search of investment opportunities. A prime example of CVC Capital Partners’ keen acumen in the IT sector is its strategic investment in Avast Software, a pioneering provider of PC security software based in the Czech Republic, a move made in March 2014. The Luxembourg-based company further proved its commitment to nurturing innovation and fostering growth in the digital industry, by co-investing with Summit Partners in AVG Technologies, a Czech cybersecurity firm, through a public-to-private leveraged buyout (LBO) transaction valued at 1.25 billion euros in September 2016. Both deals showcased the firm’s ability to identify and capitalize on the potential of promising tech companies poised for exponential growth.

Notably, the firm’s track record extends beyond investments, as exemplified by its successful exit from its investment in Formula One in July 2017, a company it had acquired in 2006. This exit marked a triumphant return for CVC Capital Partners and served as a testament to its ability to yield considerable profits for its esteemed investors.

- 4. Permira

Dry Powder: 25.06 billion EUR

HQ: London, UK

With over 500 total investments and 75 billion euros in assets under management, Permira is a renowned private equity firm recognized worldwide for its specialized knowledge and proficiency in investing in companies. Permira always looks for the opportunity to partner with disruptive technology, tech-enabled and category-creating organizations led by visionary management teams. Boasting a dry powder of 25.06 billion euros and managing 17 open funds further strengthens Permira’s reputation in the IT industry and makes the company a preferred choice for tech firms on the verge of transactions.

In a public-to-private leveraged buyout (LBO) deal worth 5.47 billion euros, Permira co-invested with Canada Pension Plan in Mimecast, a London-based leading company specializing in email security and cyber resilience. This investment demonstrates Permira’s ability to identify innovative tech firms. Besides its notable impressive investment performance, Permira has a strong history of exits, as the company has done more than 160 such transactions successfully. This expertise spotlights the firm’s commitment to generating significant returns for its investors and many well-known past and present portfolio companies, such as McAfee, Zendesk, or Hugo Boss further solidify Permira’s reputation as a premier option for tech companies in search of an investor.

- 3. Hg

Dry Powder: 25.28 billion EUR

HQ: London, UK

Hg is widely recognized as a distinguished private equity firm with a formidable track record of investing in companies poised for growth. Boasting a substantial war chest of 25.28 billion euros in unallocated capital, the firm adeptly manages a diverse portfolio of 33 open funds. Hg’s dynamic portfolio presently comprises 53 companies, collectively valued at approximately 50 billion euros in assets under management. The London-based private equity firm has a core expertise in funding and supporting businesses operating in the software and technology-enabled sectors, including software-as-a-service (SaaS), cloud computing, cybersecurity, fintech, and healthcare technology.

This deep domain knowledge and experience in the sector is showcased in Hg’s history of transactions. In March 2019, the firm invested in Transporeon, a leading cloud-based logistics platform located in Germany, through a leveraged buyout worth 706 million euros. Hg recently exited its investment in Transporeon for 1.88 billion euros, meaning that the company has now made more than 120 successful exits. Additionally, Hg has made illustrious investments in companies such as The Access Group and Visma Group, both in the IT sector. These achievements exemplify the firm’s ability to identify innovative and growth-oriented companies and provide them with support to realize their potential.

EQT

- 2. EQT

Dry Powder: 31.42 billion EUR

HQ: Stockholm, Sweden

EQT, a premier private equity firm with a global reach, is an excellent choice for tech companies seeking capital to propel their growth. Through 31 open funds the firm has a significant dry powder of 31.42 billion euros, which it uses to fund growth-oriented organizations across various industries. The Stockholm-based company is dedicated to sustainable investment and focuses on making positive environmental, social, and governance (ESG) impacts through their capital deployment. As of now EQT has close to 150 active portfolio companies, amounting to a substantial 114 billion euros in assets under management.

EQT’s investment in foodtech company SNFL Group in March 2022, a co-investment with AM FRESH Group and Paine Schwartz Partners, saw the firm lead a 1.6 billion euros growth round in the Spanish company. Two months later, EQT also made a successful exit from Wolt, a Finnish food delivery startup, after it had acquired the company in 2019. This exit emphasizes EQT’s capacity to enhance the value of its portfolio firms, in addition to its ability to deliver profitable outcomes to its stakeholders. A deep understanding of the IT industry and a proven track record of successful investments and exits means Swedish EQT is a top choice for either a buyout or a growth round.

- 1. Ardian

Dry Powder: 39.51 billion EUR

HQ: Paris, France

Ardian, one of the world’s largest private equity firms, presents a compelling choice for companies pursuing growth. With an impressive dry powder of 39.51 billion euros, the company’s investment strategy is to provide flexible capital to organizations in various industries, including IT. The firm had approximately 1,300 total investments in the past and manages 31 open funds currently. Ardian has a diverse active portfolio of around 200 companies, amounting to a staggering 130 billion euros in assets under management.

Ardian’s investments in Taxually, the Hungarian start-up providing tax reporting solutions and Poznan-based Allegro showcase the firm’s interest in the technology sector – Ardian co-invested in the Polish and European e-commerce market leader’s 3.1 billion euros buyout in January 2017, which is one of the largest transactions in the industry in the CEE region. Ardian has also made notable investments in other tech companies such as TDF Group in France or WorldPay in London.

A successful exit from Vivacom in November 2012 highlights Ardian’s ability to create value and generate substantial returns for their investors. Vivacom, a leading Bulgarian telecom operator, was sold for 1.2 billion euros, which was a significant achievement for the French private equity firm. With their knowledge and capabilities, Ardian is equipped to provide business guidance and agile capital to fund the expansion of established companies, offering the necessary support for growth.

And +1, being the most active technology PE investor in the CEE region:

- +1: MCI

Dry Powder: 51.67 million EUR

HQ: Warsaw, Poland

Web: https://mci.pl/en

As the most active technology investor in the CEE region, MCI Capital rightfully earns a place on this illustrious list. The prominent Polish private equity firm boasts a distinguished track record of over two decades in unlocking substantial value from IT investments, with a keen focus on the flourishing fintech, e-commerce, and digital media sectors (btw, we also supported our Client in an M&A deal with it). With a robust financial position, including significant dry powder of 51.67 million euros, and managing assets under management (AUM) totalling 576 million euros, MCI Capital is a formidable player in the industry.

Setting them apart is their proactive and hands-on approach with portfolio companies, characterized by strategic and operational support, leveraging their extensive network of industry contacts and resources to drive value creation initiatives. Their commitment to responsible investing is evident in their meticulous integration of sustainability and ethical considerations into their investment decision-making process, aligning with the ever-growing demand for responsible and ethical investment practices in the technology sector.

Noteworthy exits from MCI Capital’s portfolio include prominent companies such as Zettle by PayPal, Lifebrain, and Polish Allegro, underscoring their ability to deliver successful outcomes for their investments. A prime example of their expertise is their 2017 acquisition of Hungary-based Netrisk through a leveraged buyout (LBO) worth 56.5 million euros, followed by a successful partial exit just three years later, yielding a remarkable 55 million euros and retaining an approximate 24% share in the company. The Warsaw-based private equity firm managed another impressive transaction successfully in December 2018, by acquiring Polish tech company IAI SA through a public-to-private LBO. MCI Capital’s extensive experience, hands-on approach, commitment to responsible investing, and robust financial position exemplify their status as a reliable partner for technology entrepreneurs in Central and Eastern Europe (btw, we also made deal with them).

Private equity – active past years, bright future

The private equity market has a promising future, as demonstrated by its remarkable activity in 2021 and 2022. Record-breaking transaction values and volumes, driven by ample dry powder available to firms, highlight the industry’s strength and potential.

PE players have been actively utilizing their dry powder to expand their portfolio companies and drive M&A market activity, underscoring their ability to capitalize on investment opportunities. The diversification across sectors, such as healthcare, technology, energy, and real estate, further strengthens the market’s resilience and potential for sustained growth. Overall, the private equity industry is poised for a bright future, with PE firms driving M&A market activity and contributing to the industry’s ongoing success.

Term Sheet – How to Negotiate a Favourable Agreement with an Investor?

What is a Term Sheet?

The term sheet outlines the specifics, the key terms of the collaboration with a venture capital or private equity investor. First of all, it is a good sign if you got one. It may happen you received an indication of interest or LOI (letter of intent) that summarized the main terms of the offer, then you got a much more detailed term sheet.

Each term sheet is unique to the project stage, company, investor, and investment size. However, it is important to note that a term sheet is not a bank loan agreement or a "take it or leave it" set of conditions! While some terms are standard, many are negotiable—and should be negotiated.

Hundreds of businesses in the region seeking investment face the question of how to strike a good deal with an investor, protect their interests, and lay the groundwork for a successful partnership in the years to come. The process is complex, requiring both parties to reach consensus not only on critical issues like equity ownership or profit distribution but also on many other conditions.

A poorly negotiated agreement can lead to a disadvantageous and demotivating “relationship” for years instead of fruitful collaboration.

Many entrepreneurs lacking the experience in transactions tend to judge whether the term sheet is favourable based on one or two parameters — usually equity ownership and company valuation (the two is connected naturally). If the investor demands a higher equity stake or sets a lower valuation than previously expected, they consider it a bad deal. While this may seem reasonable, the term sheet contains numerous other terms that significantly influence the overall picture and can even tip the scales in a different direction. It’s worth to consider carefully which conditions genuinely provide advantages and are negotiable while avoiding unnecessary delays with terms that cannot be negotiated or won’t provide significant benefits.

In addition to determining equity ownership, there are many other factors companies should focus on—but unfortunately, they often neglect these. Let’s take a closer look at these!

Equity and Valuation – What’s the Right Balance?

It is common for companies seeking venture capital to evaluate potential investors primarily based on the equity stake they expect in return. However, both entrepreneurs and investors sometimes misguided about equity stakes. Investors often demand more equity than what would be “fair,” or even a controlling majority in the company, even though they could achieve their goals using other tools.

This issue is particularly a problem for early-stage companies, where risks are exceptionally high because there may not even be a product-market fit or sufficient market validation. Excessive equity demands can kill the founders' motivation.

What does this mean in practice?

Let’s assume the VC investor requests 40% in the first round, justifying it with reasons like high risk or uncertainty about the numbers. Depending how they forecasted the runway and which phase the company is, a new round of funding may be required. The new investor will look at the current cap table and situation and propose they need 35-40% for their significant contribution (even worse if it’s a down round). This would reduce the founders to owning just 35-40%. Should a new round come, there is not much space for the new investor left. The cap table is broken.

In many cases, an experienced VC will not invest in these cases. Even the product and team is great, if the cap table is broken, they have to pass it.

Imagine if at the end of the day the founders dilute to 10-20%... Will they be as motivated to push hard, working day and night fully committed? A subtle comment: if the first investor has anti-dilution protection, the situation becomes even more dramatic. The second investor will immediately realize that continuing discussions is pointless as the deal won’t work.

The situation is even worse if a not-so experienced investor doesn’t recognize the problem, engages in months-long negotiations, and then makes an offer that leaves the founders with only 10-20%. After months of talks and significant effort, the founders may simply reject the deal.

Good news, that experienced, “top-tier” VC investors know they can’t request more than ~10-25% in a certain round, and nowadays the terms are gravitating towards “standard” deal terms. Still, one has to be cautious.

Private equity deals are bit different as there may be buyouts in the structure or mixed (growth capital and buyout), also the company shall be in a more matured phase, making the equity stake & valuation discussions somewhat easier and more straightforward.

From the perspective of the founders or the company, it’s clearly a mistake to focus solely on valuation while failing to view the term sheet as a comprehensive package.

Even with low equity ownership, an investor may get strong control over the company's operations, significantly limit the autonomy and decision-making rights of the founders or management. Moreover, an excessively high initial valuation might complicate or even block subsequent funding rounds.

So, all in all, you should not let an investor get too many shares in the company as it can block your future rounds. On the other hand, targeting an unrealistic valuation can also backfire when things don’t go as planned and you need additional financing, but in the new environment with the actual metrics, your fair valuation is not as high as it was, so you will face a down round, that will be painful for everyone.

Absolvo’s Partner, Iván Gyurácz Németh joined HVCA Board

Iván’s role at HVCA will further strengthen the connection between the CEE region’s tech sector and the venture capital industry, fully aligning with HVCA’s mission to elevate professional standards and drive private equity growth across Hungary and Central Eastern Europe.

He thus joins the board alongside long-established investors such as Euroventures and leaders from the most active VC/PE companies, including Lead Ventures and Portfolion, working together to shape the market.

Ivan’s experience in the regional venture capital landscape, paired with his expertise in internationalization, business development, and B2B marketing / sales strategies, will be vital in bridging the gap between tech entrepreneurs and strategic investors, fostering even stronger collaboration and innovation while advancing HVCA’s objectives.

Venture Capital in general and in CEE – Key Insights for Businesses that want to boost their growth with fresh funding (Part 2)

What Are VCs Looking For?

Below are the most important factors that venture capital investors consider when evaluating an investment opportunity and making decisions. These aspects can also help you determine if your business is ready to raise capital.

• Growth Potential of the Industry and Large Market Size

Venture capital investors typically expect robust growth, which is usually achievable only in thriving industries. Facing many well-capitalized competitors that started earlier can reduce your chances. The industry must have some entry barriers to prevent new competitors from easily replicating your solution. A key factor is whether the market is large enough (TAM – Total Addressable Market). A small market limits the possibility of substantial growth, which will also restrict the exit options.

• Outstanding Growth Potential

You need a growth strategy and a well-founded, bottom-up business plan for the next 4–5 years, convincingly demonstrating to investors that the investment can achieve the expected returns (e.g., 5–10-20-50x). Identifying and analyzing risks and presenting plans to mitigate them are crucial parts of this strategy.

• Proven Market Demand and Business Model, Traction

Depending on the stage and maturity of your business, you must show different levels of “proof.” At a minimum, you need evidence and initial market feedback validating your concept. In concrete terms, you should have initial customers and sales or at least one or two pilot projects to demonstrate that your concept works and customers are willing to pay for it. If you're seeking funding for international expansion, investors will expect knowledge of the target markets, a team member capable of managing this expansion, and ideally some initial results in those markets. Being a market leader makes this process significantly easier.

• Unique Competitive Advantage, USP

A clearly defined USP (unique selling proposition) or competitive advantage is a prerequisite for a successful business and venture capital investment. The competitive advantage must be real and distinguishable—generic claims like “fast,” “efficient,” or “flexible” won’t suffice. A price advantage alone is not valuable. Furthermore, the competitive advantage must be defensible and at least sustainable in the medium term.

• Exceptional, Competent Team with a Credible Track Record

One of the core principles of venture capital is that investors bet on the jockey, not the horse. The management team is scrutinized closely, and attributes like leadership experience, prior professional achievements, and commitment are essential. For early-stage venture capital investments, the quality, composition, and dynamics of the team are often decisive factors. Investors are more likely to invest in an excellent team with an average idea than in an average team with an excellent idea because the team is what drives success.

• Scalability and International Perspective

Due to their high return expectations, venture capital investors rarely believe local CEE companies can achieve the desired growth solely in their domestic market. At least a regional, ideally global model is required. When planning expansion, carefully consider which target countries to enter, why, and how you’ll serve local customers. Other business models allow you to be born global from day one. You should not optimize for the local market, for the local customer needs. A standard Series A investment typically requires a proven, scalable acquisition channel supported by data to demonstrate that a robust system exists. For example, if €1 million is injected into the business, investors should have a clear idea of how many customers and how much revenue this will generate.

• Attractive Exit Opportunity Within ~5 Years

As mentioned earlier, venture capital is inherently exit-oriented, aiming to realize returns within 4–5 years. A business ready for this “marriage” shall have a developed exit strategy (not required in very early stage). You should showcase current M&A transactions in the industry and future potential targets, explaining why your business could become an acquisition target in a few years and identifying potential buyers.

• Soft Parameters

These include all non-quantifiable factors, such as personal impressions, feelings, and “chemistry,” which can influence the investor’s decision and, in extreme cases, even derail a transaction. Remember, venture capital investment ties both parties together for years, so mutual impressions matter. Does the other party arrive punctually for meetings? Do they take long vacations? How do they behave during informal conversations? Even seemingly trivial details—such as how you ask for coffee from the assistant —can impact an investor's perception. It’s surprising how many small things can influence an investor!

How to Prepare Before Approaching VC Investors?

The further a startup progresses on its own (i.e bootstrapping) in the implementation process, the more likely it is to capture the interest of one (or even multiple) investors. It’s rare for an investor to provide hundreds of millions of euros to finence an early-stage project still in the idea phase. This isn’t due to doubts about innovation or growth but rather the risk factors associated with early-stage ventures. Some say: Ideas are nothing, execution is key.

Once a prototype is truly functional, embraced by the market, and has achieved market traction or even a leading position, the risk decreases significantly. At that point, investors are much more willing to provide substantial funding.

It’s critical to assess how to advance your project further before approaching investors. This might include validating realistic market demand and presenting needs as accurately as possible.

For businesses that have been successfully operating for several years, thorough planning of the growth strategy and establishing a clear roadmap can support investment decisions. Every company wants to close its deal as quickly as possible. Investors want to understand what’s the story they’re investing and how they’ll get returns—there will be questions! Be proactive and prepare a business plan based on metrics ad benchmarks, covering market research findings, competitor analysis, core strategy elements, sales and marketing channels, and more.

Before reaching out to investors, you should have:

- A detailed investor presentation,

- A shorter pitch deck

- Competition analysis and summary of market research and trends

- TAM estimation

- And a business plan - at the very least

What Questions Can You Expect When Approaching Investors?

If you plan to grow further with the involvement of venture capital investors, you’ll need to provide convincing answers to questions like:

- What makes your product/solution unique, and how does it stand out from competitors?

- What are the most important market trends influencing your success?

- What regulatory challenges or risks might you face?

- Is your intellectual property protected? If not, should it be, and when?

- Which country is best to launch in first, and why?

- What market players should you expect there, and what level of demand can you anticipate?

- What is the market size (TAM)?

- What are the expected customer acquisition costs (CAC), customer lifetime value (CLV), and sales conversion rates?

- Would a joint venture, a reseller network or a local office be the better solution for you?

- What costs and returns are associated with each option?

- How will your gross margin evolve throughout the years?

- What makes your offering/solution sticky?

- Can you utilize network affects? How?

- What costs and returns are associated with each option?

- Can the business deliver above-average returns as expected by investors?

- Do you have an idea about the investor’s exit? What exit value would satisfy you?

This list is far from exhaustive. However, thorough preparation can significantly enhance the credibility of your project, increasing the likelihood of a successful fundraising process!

How Long Does It Take to Find an Investor?

Each project and investor are unique, making it challenging to estimate the time required to find the right investor. Extreme cases do exist—some companies have secured investors in just a few weeks, while others have taken more than a year. Realistically, for raising venture capital , you should plan for a process lasting 6–12 months.

The more progress you make independently (collecting feedback from the market, implementing plans beyond the concept stage, entering international markets, gathering experience, etc.), the shorter the average investment timeline can be. Involving experts can also streamline and accelerate the process. Several years of expertise and experience like Absolvo’s can significantly reduce the required preparation time.

What Does the Capital Raising Process Look Like?

You can read more about the main phases of the process here >>

The Typical Conditions of VC Investment

The details of the specific collaboration are outlined in the investor's offer (indicative offer, LOI, NBO), known as the term sheet. It is unique to each project, company, and investment.

Some parts of the term sheet are standard, but many terms are negotiable - and they should be negotiated well! Whether an investor's offer is advantageous is not solely and primarily determined by the ownership stake requested or the company valuation

- contrary to what many founders or owners might initially believe. The term sheet contains numerous additional conditions that can significantly influence the overall picture, potentially even changing the perception of the offer entirely.

For most businesses, capital raising is not an everyday task, so it's completely natural that interpreting a term sheet, evaluating its conditions, and negotiating them aren't routine activities either.

Experts in capital raising can support businesses also in this area. Up-to-date expertise, knowledge of truly "standard" conditions, experience with investors, and years of professional negotiation, and transaction experience increase the likelihood of achieving a genuinely "good deal". A poorly negotiated agreement can lock both parties into years of disadvantageous and demotivating "co-suffering" instead of a fruitful collaboration.

Just to mention a few topics:

During negotiations, can we expect the investor to waive their drag-along rights? Should we fully accept their veto rights? How should we address an early exit? What can we expect regarding liquidation preferences. Will we even receive cash at the time of exit? Is a right of first refusal key for the founders? What happens if the company needs further financing? Who should be on the board? What are the relevant reserved matters for the board and/or the shareholders meeting?

So, it is beneficial to:

- discuss these questions with an experienced advisor and prepare with their guidance.

- understand the chosen investor's preferences in advance and prepare strategically.

- have an experienced team evaluate the offer provided by the investor.

How Do You Increase Your Chances with International Investors?

- It's not enough to be good; you must demonstrate competitive advantage and a unique selling proposition (USP) on an international level.

- Your revenue likely doesn’t come solely from the domestic market anymore, proving your ability to succeed in international business development and customer acquisition.

- Your team must be capable of building an international company, ideally including foreign team members.

- You plan to establish a presence in your target market (e.g., opening an office or even relocating a founder), or even better, this process is already underway.

A common pattern is that founders have lived or worked abroad, attended foreign universities, or participated in non-local accelerator programs - showing that their ability to succeed in a foreign culture and build a successful business won’t be tested using the investor’s money.

When Is Venture Capital Not the Right Fit for You?

- If during the planning phase, it becomes evident that the project or company cannot achieve annual growth of at least 30-50% (of course depending on the basis).

- If market analysis reveals that your competitive advantage is only temporarily sustainable.

- If the market is not large enough (TAM shall be above €500Mn or even 1Bn).

- If you're not willing to sell the company after 3-5-7 years.

In these cases, it’s worth reconsidering whether your idea or plan can deliver the return investors expect. As previously mentioned, securing venture capital investment is a lengthy, time-consuming process requiring significant energy.

Additionally, Avoid Seeking Investors if:

- You need external funding immediately, as the minimum expected six-month capital raising process length is a "slow solution for you."

- If you struggle with the idea of accepting investors as co-owners, feel reluctant to give up equity—even temporarily—or allow them a say in company decisions. Getting VC money inherently means the investor will become a co-owner for a specific period, so you should be onboard with that from the beginning.

- You disagree that planning growth, developing strategies, and preparing business calculations are indispensable for securing a partner or funding for your project. These strategy-related questions will undoubtedly be asked.

Venture Capital in general and in CEE – Key Insights for Businesses that want to boost their growth with fresh funding (Part 1)

While venture capital offers opportunities to accelerate expansion, growth, the process of securing VC investment is complex. It requires an understanding of investor expectations, proper planning of strategy and financials; detailed term sheet and investment agreement negotiations.

Venture capital (VC) is an equity-based financing method, typically used by businesses with high growth potential in specific phases of their lifecycle—particularly in early and growth stages.

The financing needs and options for companies vary significantly depending on whether they are in an early- or a more mature growth phase.